As the level of technology in China's IC design industry has increased and the industry has successfully transitioned to mobile communications IC products, some of the IC design firms concerned have made extensive capital gains through IPO listings, a phenomenon that has only served to attract more China-based companies into the IC design industry. The country's total number of IC design firms had already risen to 534 in 2012, providing further evidence that the China IC design industry has apparently entered a new growth cycle.

Strong domestic demand in China has helped the China industry to avoid the worst of the inventory adjustment problems experienced by major global chip makers and the effects of the European debt crisis; the China industry's output value reached US$3.53 billion in 2012, representing 16.3% growth on the 2011 figure of US$3.04 billion.

While there is little doubt that the China IC design industry is flourishing, the actual size of its output value is less certain.

In addition to analysis and forecasts for the China foundry industry's output value in 2013, this report makes use of cost structure analysis for IC design firms in the Greater China region, calculations of Greater China-based foundry companies' revenues from the China market and of the value created by foundry companies in the Greater China region for the China semiconductor industry, to estimate the output value of the China IC design industry and the changes in this figure, as well as Greater China-based foundry companies' share of the China foundry market.

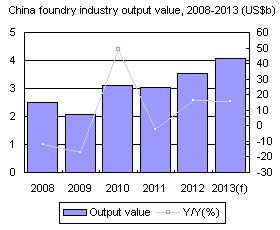

Chart 1: China foundry industry output value, 2008-2013 (US$b)

China foundry industry key strategy - Expand 12-inch capacity

Table 1: Capacity and main processes for China's major foundries, 1Q13

Chart 2: China 12-inch capacity in the foundry industry, 2011-2013 (K, 8-inch equivalents)

Chart 3: China non 12-inch capacity in the foundry industry, 2011-2013 (K, 8-inch equivalents)

Chart 4: Total capacity for the China foundry industry, 2011-2013 (8-inch equivalents0

Chart 5: 12-inch capacity as a proportion of total capacity, 2011-2013

China foundry industry will continue to expand capacity for advanced processes in 2013

Chart 6: Technical roadmaps for the major foundries in China, 2H11-2H15

Chart 7: Output value share for China foundry industry by application sector, 2011-2013

Chart 8: Output value for the China foundry industry by client, 2011-2013 (US$b)

Chart 9: Output value for the China foundry industry by process, 2011-2013 (US$b)

Chart 10: Output value share for the China foundry industry by process, 2011-2013

Chart 11: Output value for the China foundry industry by region, 2011-2013 (US$b)

Chart 12: Output value share for the China foundry industry by customer region, 2011-2013

Value created by China market for the Greater China semiconductor industry

China IC design industry has already entered a new growth cycle

Growing importance of the China market to the Greater China foundry industry

Chart 14: Taiwan foundry firms' China revenues, 2011-2013 (US$m)

Chart 15: Greater China foundry firms' revenues from the China region, 2011-2013 (US$b)

Cost structure analysis and 2013 output value forecasts for China's IC design firms

2013 market share forecasts for the major Greater China foundries

Chart 20: China market share for major foundries in Greater China, 2011-2013