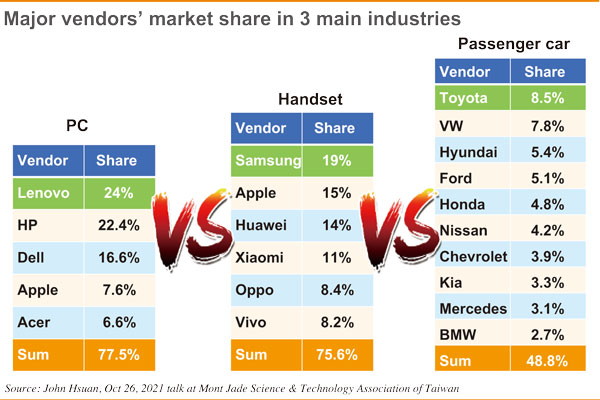

In terms of market concentration, the top-6 mobile phone brands account for 75.6% of the market, and the top-5 PC vendors have 77.5%. Both industries show a considerably stable market structure. It is a different scenario in the automotive industry though. The top-10 automakers account for only 48.8% of the market. The market leader Toyota grasps a less than 10% market share. Though none of the carmakers dominate the market, the carmaking industry is highly concentrated in major industrialized countries. For instance, the automotive industry contributes 7-10% of GDP in major industrialized countries such as the US, Germany, Japan and South Korea. For many industrialized countries, it is a global race of "sink or swim".

The conventional fuel-powered vehicles come with high industrial complexity, while the new-generation EVs tend to have much fewer mechanical parts but consist of new electronics parts like semiconductors, panels, and cameras. The cost-effectiveness and significance of batteries are exerting profound impacts on the structure of the automotive industry. What's more, EVs will be inevitably connected with V2X services. Besides the integration of hardware and software, value creation and emerging services catering to the local markets will bring more business opportunity. Not only India, Vietnam, Indonesia but Mexico and Thailand are eager to play the role of regional hubs for the automotive industry.

Among other things, state-of-the-art technologies and applications are flipping the traditional business models of the automotive industry. European automakers would usually make slight changes to the lights every three years or so and introduce a design overhaul for the chassis, body frame and engine every three to seven years. Japanese carmakers would do similar things in cycles of 1-2 years and five years, respectively. According to Bloomberg, at least 500 new EV models will be launched into the global market in 2022. The EV is becoming the third mobile computer on wheels. The vehicles will be empowered and transformed with new features by ICs and software provided by IT players from design houses to assembly and sales. The market segments and models of competition need to be re-defined.

We can foresee unlimited business opportunities brought by surging market demand satisfied by diverse and interrelated technology and services of the exuberant automotive industry.

In terms of semiconductor content per vehicle, the conventional fuel-powered vehicle uses about 40 semiconductor parts, and EV more than 150. Taiwan has the world's top-class wafer foundry underpinned by multiple capabilities of the IC design industry. The synergy created by the two sectors is second to none. Jerry Wang, general manager of Automotive Research & Testing Center, echoed UMC co-founder John Hsuan's statements saying the number of microcontrollers in a vehicle have been increased from 40 to 150-200. Automakers of Japan and South Korea have their own EV factories. For European and American automakers, the "harmless" Taiwan is their first choice for strategic partnership.

Which manufacturers will vie for this promising new market? Hsuan likened the kinds of strategic alliances among businesses to th kinds of relationships between the warlords of ancient China. He also stressed localization will be a necessary outcome.

We are talking about a mega-industry of US$2 trillion. Taiwan needs to present a big framework and take ambitious initiatives like what it did during the 3C era for its semiconductor industry to have the upper hand in the global race.

(Editor's note: This is part of a series of analysis of Taiwan's role in the global ICT industry.)