The India government began to institute the Production Linked Incentive (PLI) Scheme for Telecom and Networking Products to drive local manufacturing of telecom and networking products and build a strong 5G ecosystem.

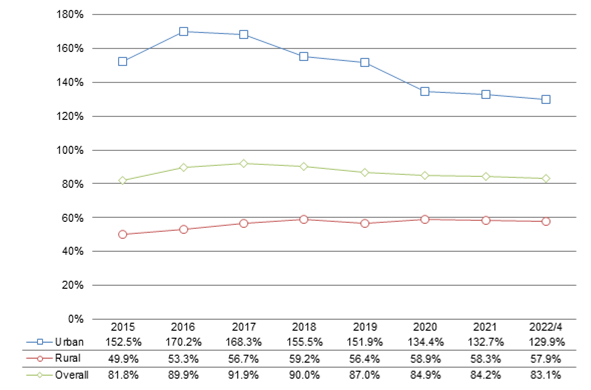

India's telecom user base reached a peak of 1.19 billion in 2017 and slipped to 1.143 billion as of April 2022. Its mobile cellular subscriptions per 100 people (tele-density) also gradually went down from 91.9% in 2017 to 83.1%. This shows that both the telecom user base and tele-density in India are reaching saturation.

High penetration of telecom services in urban areas is the main reason hindering India's telecom user base from exceeding the 1.2 billion mark. In contrast, telecom subscribers in rural India maintained above 520 million from 2018 through April 2022, higher than the levels seen in 2015 through 2017, indicating the purchasing power for mobile phones and telecom infrastructure are improving in rural India.

Chart 1: India tele-density in urban and rural areas, 2015-April 2022

Chart 2: India telecom services user number in urban and rural areas, 2015-April 2022 (m unit)

Chart 3: India Internet user number in urban and rural areas, 2015-2021 (m unit)

Chart 4: India telecom carriers revenues from wireless access business, 2015-2021 (INRb)

Chart 5: India telecom industry ARPU and share of GDP nominal per capita, 2015-2021 (INR)

Chart 6: India telecom carriers share of local telecom services users, 2015-April 2022

Introduction

India-based telecom operators generated robust revenues from access services in 2021, the highest since the commercialization of 4G in the nation, thanks to rebounding average revenue per user (ARPU) and a large telecom user base steadily exceeding 1.15 billion. The India government began to institute the Production Linked Incentive (PLI) Scheme for Telecom and Networking Products to drive local manufacturing of telecom and networking products and build a strong 5G ecosystem.

India's telecom user base reached a peak of 1.19 billion in 2017 and slipped to 1.143 billion as of April 2022. Its mobile cellular subscriptions per 100 people (tele-density) also gradually went down from 91.9% in 2017 to 83.1%. This shows that both the telecom user base and tele-density in India are reaching saturation.

High penetration of telecom services in urban areas is the main reason hindering India's telecom user base from exceeding the 1.2 billion mark. In contrast, telecom subscribers in rural India maintained above 520 million from 2018 through April 2022, higher than the levels seen in 2015 through 2017, indicating the purchasing power for mobile phones and telecom infrastructure are improving in rural India.

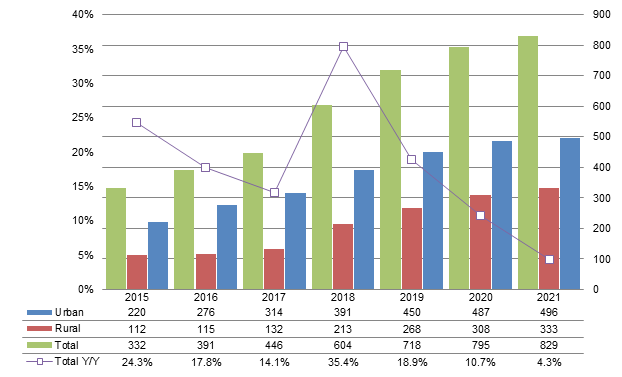

As opposed to a saturating telecom user base, India's Internet user base increased from 332 million in 2015 to 829 million in 2021, among which 803 million go online using mobile devices through wireless connections. With a growing number of mobile phone users, people in India are highly dependent on wireless communication to access the Internet.

Indian telecom operators together generated revenues of INR1.65 trillion (US$21 billion) from access services in 2021, exceeding those of 2016, the second-highest record since 4G's commercialization there. Reliance Jio is the largest telecom operator in India in terms of both subscriber base and revenue. Bharti Airtel follows closely behind with a narrowing gap and stands a chance of challenging Reliance Jio's leading position.

Based on Digitimes Research's studies, India planned to kick off 5G commercialization in 2020 but kept delaying it. The latest schedule is to roll out 5G services by year-end 2022. On the other hand, with the PLI Scheme for Telecom and Networking Products in place, aimed to promote India's manufacturing capabilities and develop a strong 5G ecosystem, eligible domestic and global manufacturers will receive incentives for five years.

Industry breakdown

Tele-density and subscribers

Compared to most developed countries that rolled out their 4G network in the early 2010s, India made slow progress. It was not until Indian oil tycoon Mukesh Ambani established Reliance Jio in 2015 and invested US$20 billion in 4G network build-up that the rest of India's telecom operators followed suit.

According to the statistics released by Telecom Regulatory Authority of India (TRAI), India's tele-density rapidly rose from 81.8% in 2015 to 89.9% in 2016 and 91.9% in 2017, mainly driven by the 4G kick-off. India's nominal GDP per capita also grew from US$1,610 in 2015 to US$2,018 in 2018, which fueled mobile phone sales in India at the time.

However, India's tele-density began to go downhill after reaching a peak in 2017, sliding to 83.1% as of April 2022, which was still higher than the 2015 level of 81.8%. India's telecom user base is already coming close to saturation before 5G commercialization. Although its GDP per capita continued to climb to US$2,037 in 2019 and US$2,111 in 2020, the growth was slowing down. Worse yet, its GDP per capita fell to US$1,968 in 2021. This does not favor mobile phone sales in India over recent years.

For urban-rural differences, India's urban tele-density plateaued in 2016 (170.2%) and 2017 (168.3%) but had come down to 151.9% in 2019, below the 2015 level of 152.5%. The reason why the country's overall tele-density could hold above the 2015 level as of April 2022 was that the rural tele-density was able to maintain steady at 58% from 2020 onwards.

Chart 1: India tele-density in urban and rural areas, 2015-April 2022

Note: Tele-density represents the number of mobile phone connections for every 100 people.

Source: TRAI; compiled by DIGITIMES Research, June 2022

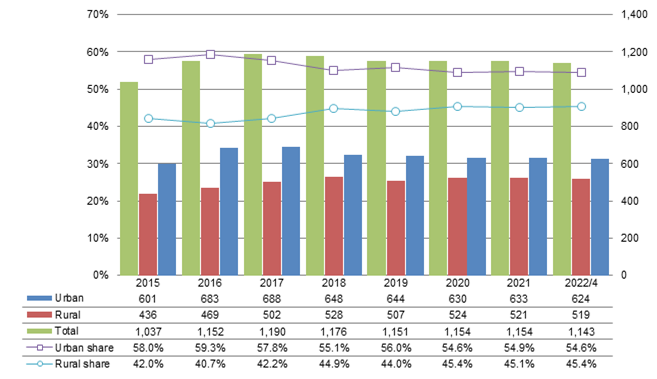

Coinciding with the changes in tele-density, India's telecom user base also reached a peak in 2017, totaling 1.19 billion, and then started to go downhill to 1.143 billion as of April 2022, still higher than the 2015 level of 1.037 billion. Its urban telecom user base began to decline in 2017 due to saturation while its rural telecom user base consistently stayed above 520 million from 2018 through April 2022. The volume exceeded the range between 436 million and 502 million from 2015 through 2017 but was not enough to drive the country's overall telecom user base to penetrate the 1.2 billion mark.

The proportion of India's urban telecom users among the country's all telecom users reached a peak of 59.3% in 2016, then quickly fell below the 2015 level in 2017 and further slid to 54.6% as of April 2022. On the other hand, the proportion of India's rural telecom users held above 45% from 2020 through April 2022, consistently higher than the levels seen from 2015 through 2019. This indicates that its rural population's purchasing power for mobile phones and its rural telecom infrastructure are both improving.

Chart 2: India telecom services user number in urban and rural areas, 2015-April 2022 (m unit)

Note: The numbers of telecom services users from 2015 to 2021 were all accumulated volumes as of year-end for the respective year.

Source: TRAI; compiled by DIGITIMES Research, June 2022

As opposed to the saturating telecom user base, India's Internet user base continued to expand from 332 million in 2015 to 829 million in 2021. In terms of the type of Internet access, 803 million users went online using mobile devices through wireless connections and only 26.58 million accessed the Internet over fixed broadband networks in 2021, indicating that Indian Internet users are highly dependent on wireless communication.

India's urban Internet user base grew at a slower pace from 487 million in 2020 to 496 million in 2021. Its rural Internet user base increased from 308 million to 333 million during the same period and the proportion among its rural telecom user base was only about 64%, meaning there is plenty of room for growth.

Chart 3: India Internet user number in urban and rural areas, 2015-2021 (m unit)

Source: TRAI; compiled by DIGITIMES Research, June 2022

Furthermore, India had only 25.16 million fixed-telephone subscriptions as of April 2022. The country is highly dependent on wireless communication whether for telephone calls or Internet access.

India telecom operators business structure

Indian telecom operators generate a majority, close to 80%, of their revenue from wireless access services, with the remaining 20% being contributed by domestic long-distance calls, international calls, as well as Internet service provider (ISP) services such as email and website hosting.

For the changes in Indian telecom operators' total access service revenue from 2015 through 2021, their revenue registered at INR1.03 trillion in 2018, which was a low point, and then started to climb thereafter. Their 2021 revenue at INR1.65 trillion set a new record, exceeding the 2016 revenue of INR1.64 trillion, which was the second-highest.

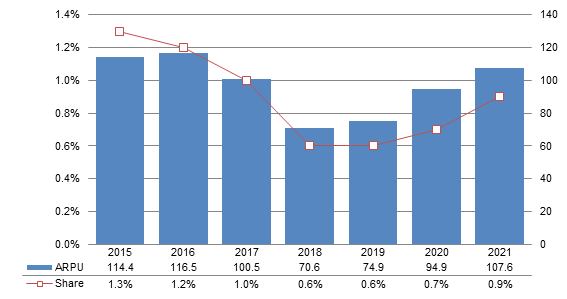

Indian telecom operators' monthly ARPU came to INR70.6 in 2018, which was also a low point, and then continued to rebound to INR107.6 in 2021, still short of the peak of INR116.5 seen in 2016. Nevertheless, the 1.154 billion telecom user base in 2021, exceeding the 1.152 billion telecom user base in 2016, drove Indian telecom operators' total access service revenue to a new high.

Chart 4: India telecom carriers revenues from wireless access business, 2015-2021 (INRb)

Source: TRAI; compiled by DIGITIMES Research, June 2022

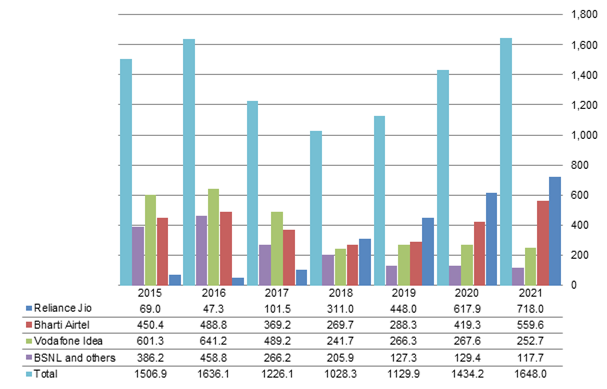

As to the changes in Indian telecom operators' monthly ARPU from 2015 through 2021, their monthly ARPU could hold above INR114 in 2015 and 2016 when 4G services went into operation but then declined to INR100.5 in 2017 with intensifying competition. This prompted a series of mergers and acquisitions among telecom companies, including Reliance Jio's takeover of Sistema Shyam Teleservices (SSTL) in November 2017 and Vodafone's takeover of Idea in August 2018.

Reliance Jio marketed 4G-enabled low-cost smartphones under its brand to encourage Indian consumers to go online and aggressively expand its market footprint. Despite a late start, Reliance Jio was able to secure a 32.1% share of India's telecom user base in 2019, surpassing Vodafone Idea's 28.9% share for the first time to sit at No. 1. However, the intense competition also caused Indian telecom operators' monthly ARPU to fall short of INR75 in 2018 and 2019, a relative low point.

As India's nominal GDP per capita grew from US$1,610-US$1,768 in 2015-2017 to US$2,018-US$2,111 in 2018-2020, the percentage of Indian telecom operators' monthly ARPU in India's nominal GDP per capita fell from more than 1% in 2015-2017 to a low point of 0.6% in 2018-2019.

Indian telecom operators' monthly ARPU representing a declining percentage of India's nominal GDP per capita may help ease the burden of telecom services on Indian citizens. However, compared to its five neighboring ASEAN countries, India's percentage of telecom operators' monthly ARPU in its nominal GDP per capita from 2018 through 2019 was only higher than Singapore's, about the same as the Philippines', and lower than Malaysia's, Thailand's and Indonesia's. This made Indian telecom operators realize that they need to moderately raise their ARPU.

Given this, Indian telecom operators began to actively encourage their subscribers to upgrade to 4G services in 2020. Their ARPU, therefore, rebounded above INR100 in 2021. Moreover, they are likely to raise their fees by the fourth-quarter of 2022.

Chart 5: India telecom industry ARPU and share of GDP nominal per capita, 2015-2021 (INR)

Source: TRAI and CEIC; compiled by DIGITIMES Research, June 2022

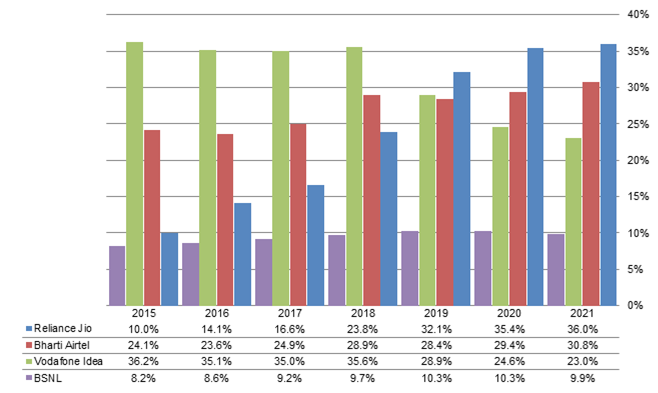

Concerning the changes in Indian telecom operators' shares of the country's telecom user base, Reliance Jio's share expanded from 32.1% in 2019 to 35.4% in 2020 and 36% in 2021, sitting at No. 1 three years in a row, but the growth was slowing down.

India's second-largest telecom operator Bharti Airtel saw its share rise from 28.4% in 2019 to 30.8% in 2021. Not only did its share grow at the rate of more than one percentage point a year, but it also reached 31.6% in April 2022. Its gap with Reliance Jio has narrowed from more than 5 percentage points in 2020 and 2021 to 3.9 percentage points. Bharti Airtel has an increasing chance of dethroning Reliance Jio.

In comparison, although Vodafone Idea stayed at No. 1 with an over 35% share from 2015 through 2018, in the face of the price competition against Reliance Jio, Vodafone Idea suffered operating losses and rumor has it that Vodafone Idea is exiting the Indian market, which is of no help to boosting its user base. Its share took a sharp downturn to 28.9% in 2019 and kept sliding to 22.7% as of April 2022, making it fall to No. 3 starting 2020.

Chart 6: India telecom carriers share of local telecom services users, 2015-April 2022

Source: TRAI; compiled by DIGITIMES Research, June 2022

Reliance Jio's access service revenue reached INR718 billion in 2021, the first among the pack to break through the INR700 billion mark. Bharti Airtel and Vodafone Idea trailed behind with INR559.6 billion and INR252.7 billion. Their revenue rankings are highly correlated to their rankings by their share of India's telecom user base.

India 5G deployment

India originally set the goal of starting 5G commercialization in 2020 but kept delaying it for several reasons including excessively high 5G auction prices that deterred telecom operators from participating in the bidding. The India government held another round of 5G auctions in second-quarter 2022 but still, no telecom operators joined the bidding. As such, the India government will lower the auction prices and schedule a new round for the third quarter. If everything is according to plan, India can expect to kick off 5G services in some densely populated urban areas by year-end 2022.

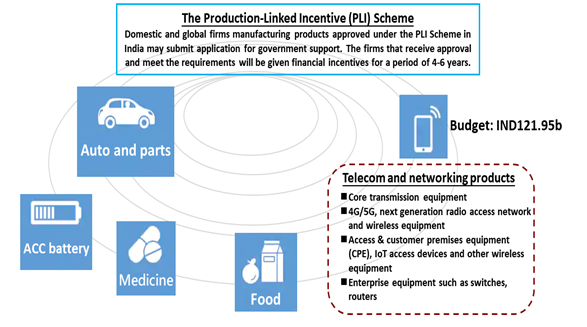

The India government announced the PLI Scheme for Telecom and Networking Products in February 2021, intending to build a strong 5G ecosystem. The PLI Scheme allocated an INR121.95 billion budget to support local manufacturing of telecom and networking products by domestic and global manufacturers. Eligible manufacturers will receive incentives for five years.

The PLI Scheme aims to enhance India's manufacturing capabilities by providing incentives to drive investment and production of exports. As part of the PLI Scheme, the India government announced an outlay of INR1.97 trillion in November 2021 for 13 sectors, extending beyond telecom and networking products to include automobiles and auto components, pharmaceutical drugs and food products.

For the telecom and networking sector, four categories of products are approved under the PLI Scheme, among which the category of core transmission equipment includes Dense Wavelength Division Multiplexing (DWDM), Optical Transport Network (OTN), Multi-Service Provisioning Platform (MSPP), Synchronous Digital Hierarchy (SDH), Packet Transport Network (PTN), Multi-Protocol Label Switching (MPLS), Gigabit Passive Optical Networks (GPON)/Next Generation-Passive Optical Network (NG-PON) and Optical Line Terminal (OLT) devices.

The category of 4G/5G, next-generation radio access network and wireless equipment includes LTE/5G Radio Access Network (RAN) base station and core equipment as well as edge and enterprise equipment. The other two categories are access and customer premises equipment (CPE), IoT access devices and other wireless equipment as well as enterprise equipment: switches, and routers.

Table 1: India government PLI scheme

Note: The PLI Scheme covers 13 sectors, including the five listed above as well as wireless production management and specialty electronics components, white goods, solar PV modules, specialty steel, textile products and electronic/technology products.

Source: Press Information Bureau India, Invest India; compiled by DIGITIMES Research, June 2022

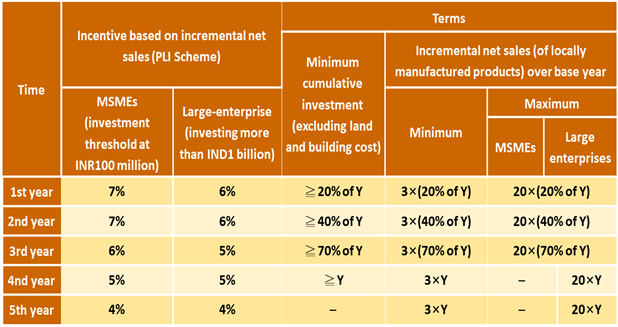

Under the PLI Scheme for Telecom and Networking Products, firms are categorized into medium and small-scale enterprises (MSMEs) and non-MSMEs, with the required investment threshold being fixed at INR100 million for MSMEs and INR1 billion for non-MSMEs. The PLI Scheme will provide the firms that meet the requirements an incentive of 6% to 7% on incremental net sales (over the base year) for the first three years and an incentive of 4% to 5% on incremental net sales for the fourth and fifth year.

Eligibility under the PLI Scheme for Telecom and Networking Products is subject to thresholds of incremental investment and incremental net sales of manufactured goods. The cumulative investment over the first three years by MSMEs and non-MSMEs must be greater than or equal to 20%, 40%, and 70% of the committed total investment by the firm over four years, and all the investments must be completed within four years.

India's financial year runs from 1 April to 31 March the following year. If firms apply for incentives under the PLI Scheme with 2022 as the first year, the base year is 2021. The Scheme stipulates that the incremental net sales of goods manufactured locally by MSMEs and non-MSMEs must be at least three times the required cumulative investment for the year. The maximum eligible incremental net sales are 20 times the required cumulative investment for the year for first three years and there is no maximum for MSMEs for the fourth and fifth years.

For example, if an MSME in the PLI Scheme for Telecom and Networking Products is committed to investing INR100 million from 2022 through 2026, its investment in 2022 will have to be higher than INR20 million and its incremental net sales of products (manufactured locally) in 2022 from 2021 will have to be more than INR60 million for the MSME to be eligible for an incentive that is 7% of the incremental net sales, i.e. INR4.2 million. The maximum incentive will be INR28 million (INR20 million x 20 x 7%). Its cumulative investment in 2023 will have to be higher than INR40 million and its incremental net sales in 2023 from 2021 will have to be more than INR120 million for the MSME to be eligible for an incentive that is 7% of the incremental net sales from 2022.

Table 2: India government PLI scheme details

Note: Y equals total committed investment for the first four years.

Note: MSMEs are medium and small-scale enterprises defined by the India government.

Source: Invest India, Invest India; compiled by DIGITIMES Research, June 2022

As of the end of October 2021, a total of 31 companies were approved under the PLI Scheme for Telecom and Networking Products, including 16 MSMEs, eight large-scale Indian corporations and seven global companies encompassing Foxconn, Xinxing as well as Nokia Solutions and Networks.

The India government announced in June 2022 an extension of the PLI Scheme for Telecom and Networking Products by one year. The duration was from April 2021 to March 2026. Firms submitting new applications may be eligible for incentives for the period between April 2022 and March 2027. Those already approved may choose 2021 or 2022 to be the base year.

Summary

India's telecom user base and tele-density both reached a peak in 2017, respectively at 1.19 billion and 91.9%, but then took a downturn to 1.143 billion and 83.1% as of April 2022. With its urban telecom user base and tele-density both reaching saturation, increasing telecom user base and mobile phone purchasing power in rural India could hardly spur overall growth for the country.

Indian people are highly dependent on wireless communication for Internet access. Indian telecom operators' access service revenue reached a new peak in 2021 since 2015 mainly as they had come to realize the need to moderately raise their ARPU and succeeded at doing so by driving users to upgrade to 4G services starting 2020.

Based on Digitimes Research's studies, India is the world's second-largest telecom market. The India-China border clash in Galwan Valley prompted India to block the use of 5G equipment from Huawei and other Chinese suppliers. The PLI Scheme for Telecom and Networking Products being promoted by the India government is expected to attract more global conglomerates such as Ericsson and Samsung Electronics to step up their investment in India.