Table 1: Key factors affecting tablet shipments in 1Q17 (Supply)

Table 2: Key factors affecting tablet shipments in 1Q17 (Supply)

Table 3: Key factors affecting tablet shipments in 1Q17 (Demand)

Chart 2: Shipments by product- iPad, non-iPad branded and white-box, 4Q15-1Q17 (m units)

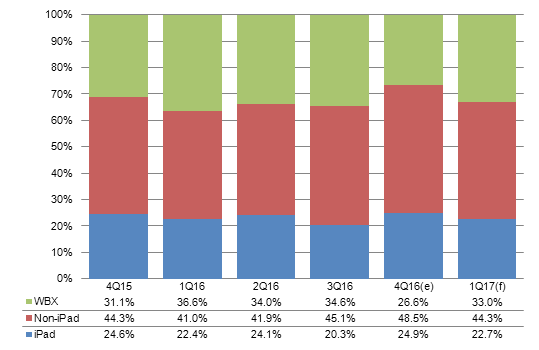

Chart 3: Shipment share by product - iPad, non-iPad branded and white-box, 4Q15-1Q17

Chart 8: Shipments by touchscreen technology, 4Q15-1Q17 (m units)

Chart 9: Shipment share by touchscreen technology, 4Q15-1Q17

Chart 14: Intel tablet shipments and share by OS, 2Q16-1Q17 (m units)

Chart 15: Shipments of detachable notebooks by OS, 4Q15-1Q17 (k units)

Chart 16: Shipment share of detachable notebooks by OS, 4Q15-1Q17

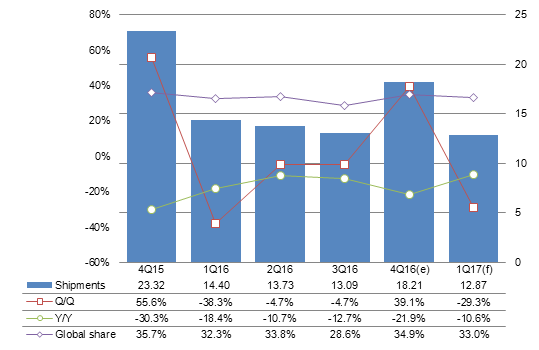

Chart 17: Shipments from Taiwan makers and share of global shipments, 4Q15-1Q17 (m units)

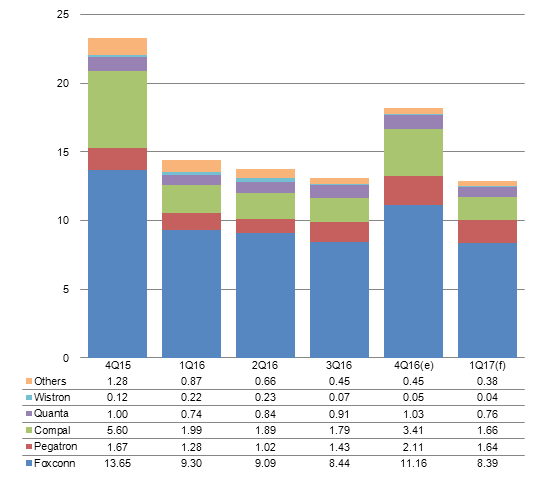

Chart 18: Taiwan tablet shipments by maker, 4Q15-1Q17 (m units)

Introduction

A shortage of key components such as panel, processor and memory reached a peak in October 2016 hence bringing tremendous stress to the global tablet market especially to manufacturers in the fourth quarter of 2016. In particular, white-box makers suffered the most as many could not meet scheduled delivery dates for potential customers. On the other hand, brands such as Apple, Lenovo and Microsoft saw their shipments perform better than expected. Digitimes Research believes total global tablet shipments in 2016 were 183 million, a 15.1% fall on year.

Moving toward the first quarter of 2017, many heavyweights plan to introduce new products in this quarter such as Apple's 10.5-inch iPad Pro and the lower priced 9.7-inch iPad, Samsung Electronics will have its high-end Galaxy Tab S3 and Microsoft has the Surface Pro 5. However, due to factors such as the low season, white-box market shrinkage, and component price increases compared to first-quarter 2016, global tablet shipment growth will be curbed. In the first quarter of 2017 global tablet shipments are expected to be only 39.03 million units, falling under 40 million units for the first time and will show an on-quarter drop of 25% and an on-year drop of 12%.

Leading the shipments is Apple and it plans to introduce three new iPads at the end of the first quarter of 2017, which will help ease seasonality effects. The vendor's first-quarter shipments are expected to reach close to nine million units. Samsung plans to introduce new high-end products that use AMOLED panels in the first quarter of 2017. The firm also plans to introduce the new Windows 2-in-1 tablet in the first quarter of 2017, but the high price will likely limit shipment growth. Lenovo hopes to return to third place in the market but Huawei plans to use a strategy of expanding shipments of all levels of tablets with phone features that use Qualcomm solutions. This will likely put great stress on Lenovo.

Key factors affecting tablet shipments in 1Q17

Supply side

Apple's shipments of the 9.7-inch iPad Pro in the fourth quarter of 2016 were better than expected bringing total fourth quarter 2016 shipments to 13 million units.

The firm plans to introduce three new products at the end of the first quarter of 2017. There will be a new 10.5-inch iPad Pro and 9.7-inch models with a lower price point, while the 12.9-inch iPad Pro will also get a new version.

Nevertheless, shipments are not expected to increase until the second quarter of 2017.

Amazon's shipments in the fourth quarter of 2016 were not as strong as before for the firm, as it stopped focusing only on shipment numbers in the fourth quarter. The firm promoted its 8-inch model during the strong holiday season so the overall average selling price (ASP) for the vendor increased. Inventory levels of the 8-inch model in the first quarter of 2017 are relatively low so shipments may outperform 7-inch models.

Microsoft's Surface showed strong shipments both in the consumer and the corporate markets in the fourth quarter of 2016 so overall shipments in 2016 are likely to be flat compared to 2015. Surface Pro, which is expected to use Kaby Lake, will see small volume shipments in the first quarter of 2017.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, March 2017

Supply side 2

Pricing of main components reached an all-year high at the beginning of the fourth quarter of 2016 and after November, panel prices began to fall which helped downstream firms but demand also fell as the holiday season ended.

Prices of 7-inch panels fell more than 20% from peak as China-based firms began dumping hoarded inventories in mid-November. The price of DDR DRAM still increased by a single-digit percentage point in the fourth quarter of 2016.

Pricing of eMMC and copper clad laminated substrates was relatively stable in the fourth quarter. The price of panels showed a slight increase in January 2017 but is expected to be flat or fall slightly in February and March.

Due to the component shortage, white-box makers faced issues with meeting demand for Wi-Fi tablets, Windows tablets, and tablets with phone features in the fourth quarter of 2016. Prices of components will remain high in the first quarter of 2017 and it will continue to negatively affect white-box makers.

Intel's SoFIA and Bay Trail exited the market completely after the fourth quarter of 2016 while prices for Cherry Trail 8300 and the new Apollo Lake increased significantly, which will affect white-box maker's costs of Windows tablets.

Makers of tablets with phone features are expected to turn to Spreadtrum's cheap solutions for 3G products while with rising demand, 4G models are likely to see an increased shipment share.

Note: The more stars, the higher the influence. ↓indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, March 2017

Demand side

The first quarter of 2017 is likely to be the quarter with the weakest demand in 2017 but as Apple, Samsung and Microsoft all plan to introduce important new products in this quarter, the low season effect may be diminished a bit.

Apple expects to lower its entry-level 9.7-inch iPads to US$299/unit and this may stimulate demand for the product and curb sales of the iPad mini series at the same time.

Note: The more stars, the higher the influence. ↓ indicates negative influence, ↑indicates a positive influence.

Source: Digitimes Research, March 2017

Shipment breakdown

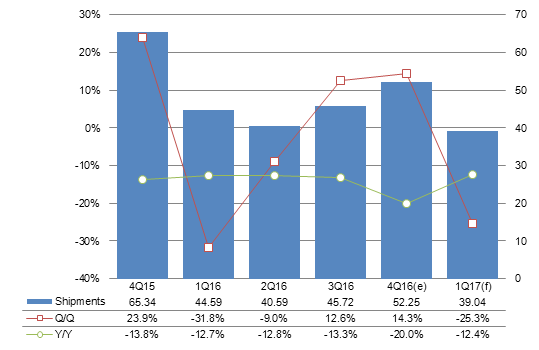

In the fourth quarter of 2016, global tablet shipments reached 52.25 million units, showing on-quarter growth of 14.3% which is better than expected. However, the figure represented an on-year decrease of 20%.

White-box makers saw shipments total less than expected due to component shortages that lasted into November, plus there were falling orders from Europe- and US-based retailers. However, brands such as Apple, Lenovo and Microsoft saw shipments that were stronger than expected.

Expected shipments in the first quarter of 2017 will be 39.03 million units, falling under 40 million units for the first time but the on-quarter and on-year decrease will both be less severe compared to the on-quarter and on-year decrease seen in first-quarter 2016.

The first quarter is a traditional low season but US- and South Korea-based brands plan to introduce new products in this quarter and this may slightly weaken the negative effect of the low season. In addition to the move up of the launch schedule of new products from US- and South Korea-based brands, the new products are also more exciting compared to new products launched in 2016.

In 2016, Apple only introduced a 9.7-inch iPad Pro but the firm plans to introduce three new products in the first quarter of 2017. Samsung's S series and Microsoft's Surface Pro did not go through any revision or enhancement in 2016.

The positive effects of the new products may show up more strongly in second-quarter 2017.

Chart 1: Global tablet shipments, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Shipments by product

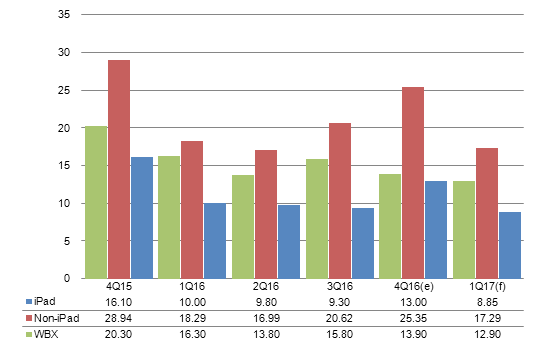

Shipments of the iPad in the fourth quarter of 2016 reached 16 million units, better than expected. The total was mainly due to 4.5 million shipments of the 9.7-inch iPad Pro, a total that was two million more than expected.

The consumer and corporate markets began to increase demand for handwriting features on tablets in the fourth quarter of 2016 so demand for the iPad Pro increased.

Shipments of the iPad in the first quarter of 2017 will likely experience less severe on-quarter and on-year drops compared to the on-quarter and on-year drop seen in first-quarter 2016.

Apple will introduce three new products in the first quarter which will help offset low season effects..

Non-Apple brands totaled shipments of 25.35 million in the fourth quarter of 2016. The figure is slightly better than expected. This was mainly due to a strong performance by Lenovo and Microsoft.

In the first quarter of 2017 shipments from non-Apple brands are expected to reach 17.28 million units with an on-quarter drop similar to Apple's. However, the on-year drop will only be 5.5%, which is better than the on-year drop of 11.5% expected for Apple. This is mainly due to Samsung and Microsoft introducing new products in the first quarter of 2017 and Huawei and Amazon are expected to show on-year growth in their first quarter 2017 shipments.

In the fourth quarter of 2016, white-box makers saw shipments only reach 13.90 million units, less than shipments in first-quarter 2016. In fact, the shortage was already felt at the end of the third quarter. September is originally a shipment peak month for white-box makers but due to a shortage of key components, such as processors and panels, shipments were much lower than expected. Digitimes Research has therefore revised its white-box shipments totals for third-quarter 2016 from 17.90 million units to 15.80 million units.

The component shortage caused unstable shipments before mid-November while demand rapidly fell after mid-November as the hot season wound down. In the first quarter of 2017 shipments from white-box makers are expected to show an on-quarter drop of only 7.2% but the on-year drop is expected to exceed 20%. This is due to the low base in the fourth quarter of 2016 and stabilized component prices.

Chart 2: Shipments by product- iPad, non-iPad branded and white-box, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Chart 3: Shipment share by product - iPad, non-iPad branded and white-box, 4Q15-1Q17

Source: Digitimes Research, March 2017

Shipments by vendor

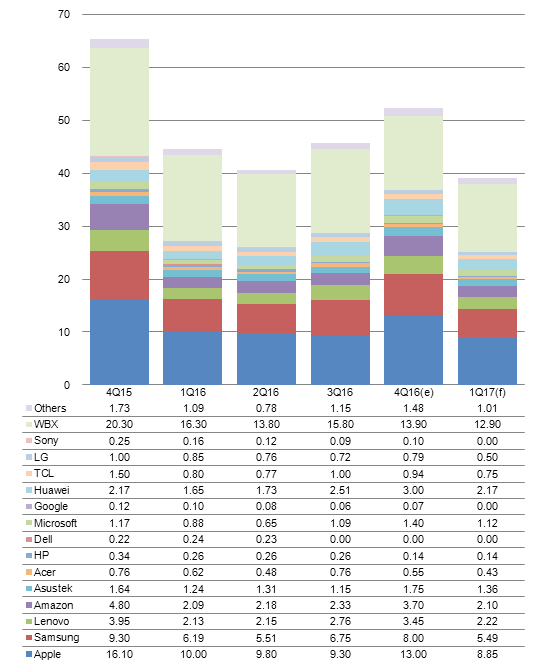

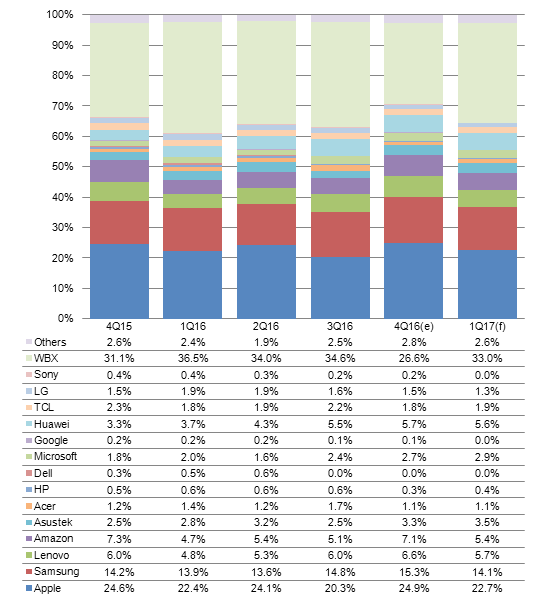

Ranking by shipments in the fourth quarter of 2016 were similar to expectations but as white-box makers saw weak shipments, the top five brands saw their shipment share increase.

In the fourth quarter of 2016, Apple saw shipments of the 9.7-inch and the iPad mini show an on-quarter increase and despite the fact that total shipments were lower compared to fourth-quarter 2015, the shipment share increased due to the significant shipment share drop of white-box makers.

Samsung focused its shipments on the entry-level to mid-range A series in the fourth quarter of 2016 but due to the Note scandal, its shipment share only increased by 0.5pp (percentage points) compared to third-quarter 2016.

Amazon focused shipments on both the 7- and the 8-inch price-friendly models with shipments exceeding 3.5 million units in the fourth quarter of 2016, hence its shipment share increased by 2pp compared to third-quarter 2016.

Due to the November 11 Singles Day in China, and a strategic alliance with BOE and cooperation with Wal-Mart on holiday sales, Lenovo saw shipments trail only slightly behind Amazon's in the fourth quarter of 2016.

Even though Microsoft did not introduce new models for its Surface Pro series, the firm continued with the promotion of the product in the corporate and consumer markets, pushing shipments to increase in the fourth quarter of 2016.

As the market enters the first quarter of 2017, which is traditionally a low season in North America, Amazon's ranking is expected to drop from third to fifth while Lenovo and Huawei will both increase by one spot.

With new products, Apple is expected to see an increased shipment share in the first quarter of 2017 compared to first-quarter 2016.

Despite the fact that Amazon's shipment share is expected to show a slight decrease in the first quarter of 2017 compared to the fourth quarter of 2016, the shipment share is expected to show an increase compared to first-quarter 2016.

Shipments of the 7-inch model are unlikely to be as strong as in 2016 but the 8-inch will likely replace the 7-inch model to become the product with the strongest shipments. This is likely to push Amazon's first quarter 2017 shipments to be comparable to shipments in first-quarter 2016.

Samsung will introduce the high-end 9.7-inch Tab S3 and the 12-inch Tab Pro S2 in the first quarter of 2017 and the shipment share is likely to show an increase compared to first-quarter 2016.

Benefitting from the Lunar New Year holiday sales and full strength to achieve its fiscal year goals, Lenovo is expected to see its first quarter of 2017 shipment share show an increase compared to first-quarter 2016.

Huawei introduced 8-inch entry-level to mid-range models using Qualcomm's APs at the end of the fourth quarter of 2016 and shipments are likely to show an increase in the first quarter of 2017. Due to the decrease of overall ASPs benefitting overall shipments, Huawei is expected to show the smallest on-quarter decrease of shipment share among the top five firms in the first quarter of 2017.

Chart 4: Shipments by vendor, 4Q15-1Q17 (m units)

Note: Google and its brand vendor partners' jointly developed tablets are included in Google's shipments

Source: Digitimes Research, March 2017

Chart 5: Shipment share by vendor, 4Q15-1Q17

Note: Google and its brand vendor partners' jointly developed tablets are included in Google's shipments

Source: Digitimes Research, March 2017

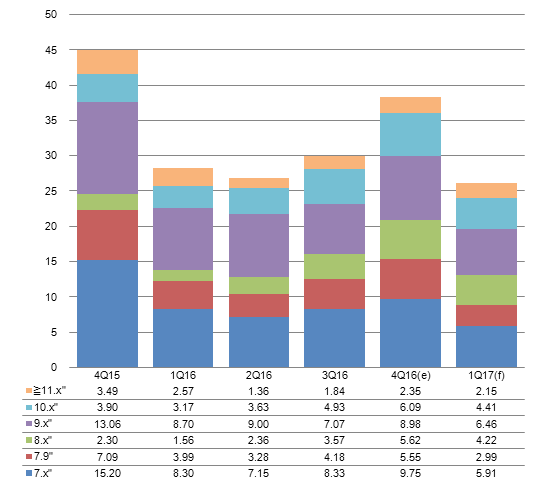

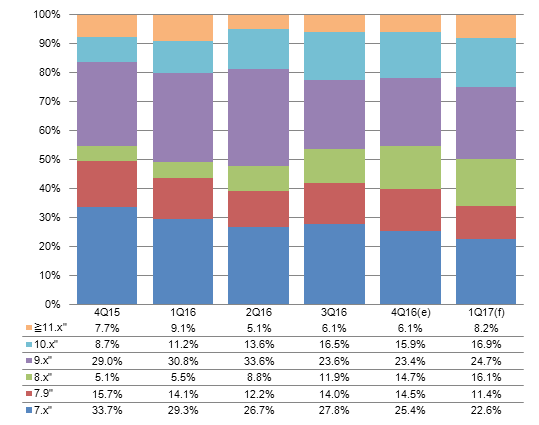

Shipments by panel size

The shipment share of 8.x-inch models reached a new high in the fourth quarter of 2016 while the shipment share of the 10.x-inch showed a slight decrease.

The 7-inch segment did not break through the 30% shipment share goal and actually saw its shipment share decrease. This is due to the fact that brands have shifted their focus to 8-inch models.

The shipment share of 9.7-inch models did not show an on-quarter increase, it was also smaller compared to fourth-quarter 2015, this was mainly because Apple did not introduce new products in the fourth quarter of 2016.

In the first quarter of 2017, the shipment share of 8-inch and the 10-inch models will likely reach new peaks while the shipment share of the 7-inch and the 7.9-inch will show a significant decrease. The 8-inch model is also the focus for Amazon and China-based brands in the first quarter of 2017.

In addition to new high-end models, Samsung also plans to introduce price-friendly mainstream 10-inch models in the first quarter of 2017. Apple also plans to begin mass production of its 10.5-inch model at the end of the first quarter of 2017.

The price of the 9.7-inch iPad is likely to fall to US$299/unit and this is expected to compress the market room for the 7.9-inch iPad mini.

Chart 6: Shipments by panel size, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Chart 7: Shipment share by panel size, 4Q15-1Q17

Source: Digitimes Research, March 2017

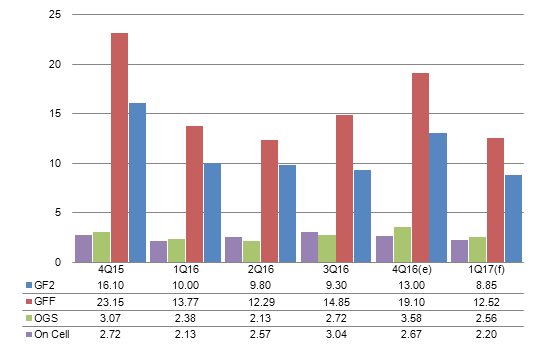

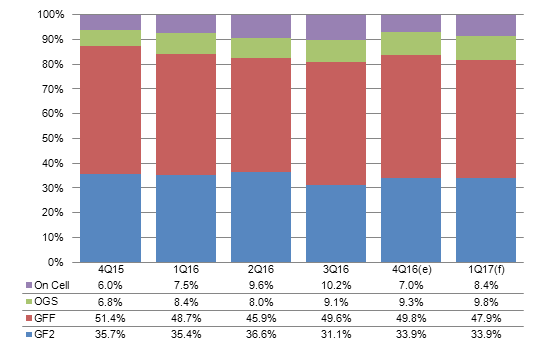

Shipments by touchscreen technology

The on-cell touch technology shipment share fell significantly in the fourth quarter of 2016 because of strong shipments of iPad (uses GF2) and Fire (uses GFF).

OGS share is expected to increase by 10pp in the first quarter of 2017.

The main reason is most of the large-size Windows tablets to be launched in the first quarter of 2017 use OGS technology.

GFF technology is expected to see its first quarter of 2017 shipment share fall by 1.9pp compared to the fourth quarter of 2016 due to the expected falling shipments of Amazon's tablets.

Chart 8: Shipments by touchscreen technology, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Chart 9: Shipment share by touchscreen technology, 4Q15-1Q17

Source: Digitimes Research, March 2017

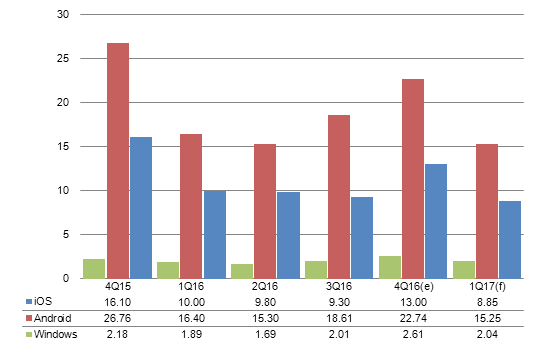

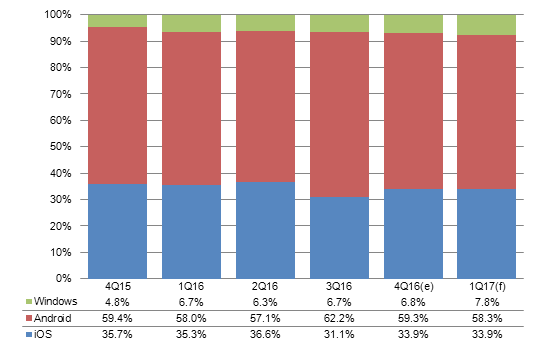

Shipments by OS

In the fourth quarter of 2016, iOS models showed shipment share growth compared to third-quarter 2016, as sales of the 9.7-inch iPad Pro and iPad mini in the holiday season in mature markets were better than expected.

In the first quarter of 2017, the shipment share of iOS models is expected to be comparable to the fourth quarter of 2016 mainly due to the launch of new iPads.

In the first quarter of 2017, the shipment share of Windows models will likely show an on-quarter increase of 1pp mainly because firms such as Microsoft, Samsung and Huawei all plan to introduce new models.

Chart 10: Shipments by OS, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Chart 11: Shipment share by OS, 4Q15-1Q17

Source: Digitimes Research, March 2017

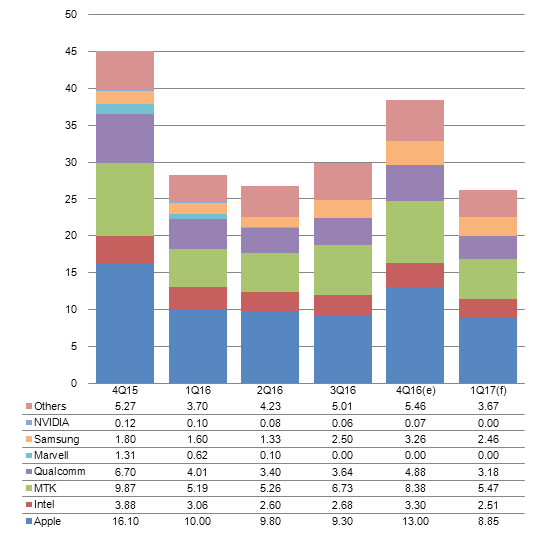

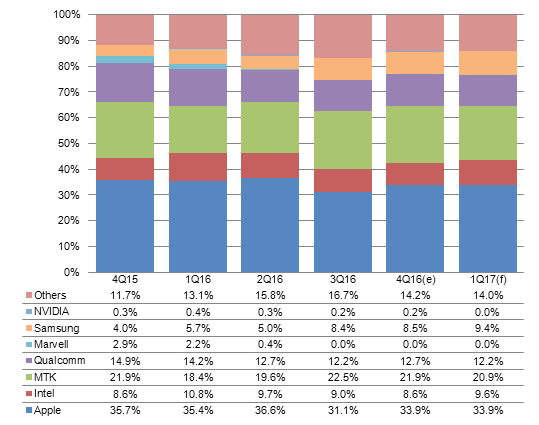

Shipments by AP supplier

In the fourth quarter of 2016, the AP ranking was similar to third-quarter 2016 and in particular, Apple, Qualcomm and Samsung all saw slight increases in their respective shares.

Qualcomm saw a share increase mainly because Samsung, Huawei and Asustek all increased the percentage of Qualcomm processors in their new tablets.

Intel saw its share in the fourth quarter of 2016 fall but the share of Windows OS increased and this is mainly due to the exit of the Android platform based SoFIA processor.

In the first quarter of 2017, the ranking is expected to be similar compared to the fourth quarter of 2016 but Intel and Samsung are expected to see an increased share.

Products that are expected to use Intel processors such as Surface Pro 5, Samsung Tab Pro S2 and Huawei Matebook 2 are scheduled to be launched in the first quarter of 2017.

MediaTek will see its share fall close to 1pp in the first quarter of 2017 compared to the fourth quarter of 2016. This will mainly be due to Amazon Fire tablet shipments that are expected to fall by 1.5 million units in the first quarter of 2017.

Chart 12: Shipments by AP supplier, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Chart 13: Shipment share by AP supplier, 4Q15-1Q17

Source: Digitimes Research, March 2017

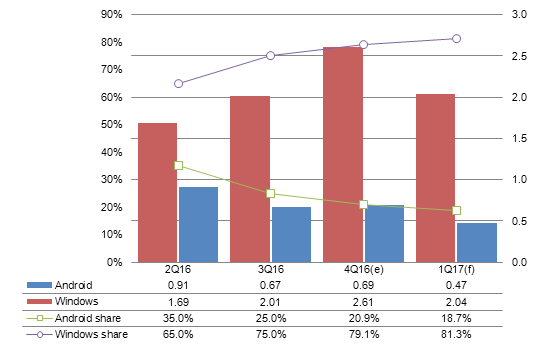

Shipments of Intel-based tablets by OS

Chart 14: Intel tablet shipments and share by OS, 2Q16-1Q17 (m units)

Source: Digitimes Research, March 2017

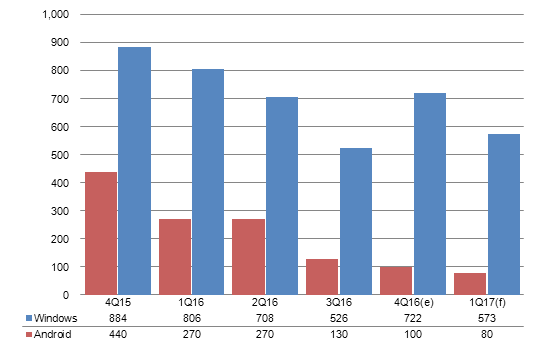

Shipments of detachable notebooks by OS

Chart 15: Shipments of detachable notebooks by OS, 4Q15-1Q17 (k units)

Source: Digitimes Research, March 2017

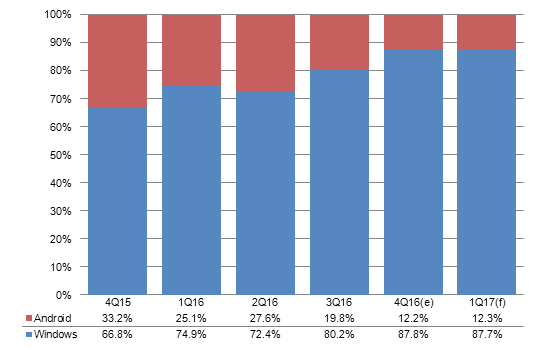

Chart 16: Shipment share of detachable notebooks by OS, 4Q15-1Q17

Source: Digitimes Research, March 2017

Shipments from Taiwan makers

The performance of Taiwan-based makers in the fourth quarter of 2016 was better than expected but compared to fourth-quarter 2015, shipments showed a more than 20% drop, the highest drop in recent years.

Despite the drop, Taiwan-based makers saw their global shipment share increase by 3.7pp on quarter in the fourth quarter of 2016 mainly due to the increase in iPad shipments. Although iPad did not have new products, due to promotional deals on the retailer side, sales were better than expected.

Despite the fact that there will be new iPads launched in the first quarter of 2017, the low season factor will still affect shipments from Taiwan-based firms hence shipments are expected to fall below 13 million units, a new record low.

However, Taiwan-based makers are likely to see their share increase in the first quarter of 2017 as shipments of iPads are likely to outperform that of China- and South Korea-based firms.

Chart 17: Shipments from Taiwan makers and share of global shipments, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

Foxconn benefitted from the significant shipment increase of the 9.7-inch iPad Pro but the maker's increase is not as significant compared to Compal and Pegatron, hence the firm's share in the fourth quarter of 2016 showed an on-quarter decrease of 3.2%.

In the first quarter of 2017, mass production of 10.5-, 12.9- and 9.7-inch new iPads will begin hence Foxconn is expected to see a share increase on quarter by 3.9%.

Compal saw its fourth quarter 2016 share increase significantly by 5pp on quarter due to strong shipments of the iPad mini 2 and 8-inch Fire tablets. Shipments of Fire tablets in the first quarter of 2017 are expected to be flat compared to the fourth quarter of 2016, but shipments of iPad mini 2 are expected to fall due to the launch of the price-friendly 9.7-inch model. Therefore, Compal is expected to see its first quarter of 2017 share drop by 5.8pp on quarter.

Pegatron benefitted from an on-quarter increase of 300,000 units of the Surface series in the fourth quarter of 2016, hence its share increased by 0.7pp on quarter. The Surface Pro 5 is expected to begin mass production in the first quarter of 2017, hence Pegatron is expected to see its shipment share increase by 1.1pp.

Unlike Compal and Pegatron, Quanta Computer and other firms saw their fourth quarter of 2016 share drop.

Chart 18: Taiwan tablet shipments by maker, 4Q15-1Q17 (m units)

Source: Digitimes Research, March 2017

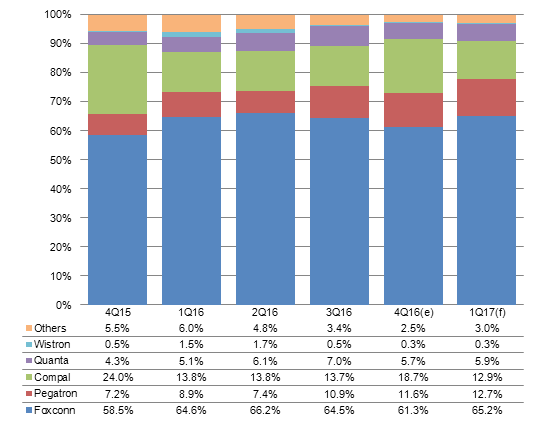

Chart 19: Taiwan tablet shipment share by maker, 4Q15-1Q17

Source: Digitimes Research, March 2017

Article edited by Michael McManus