Introduction

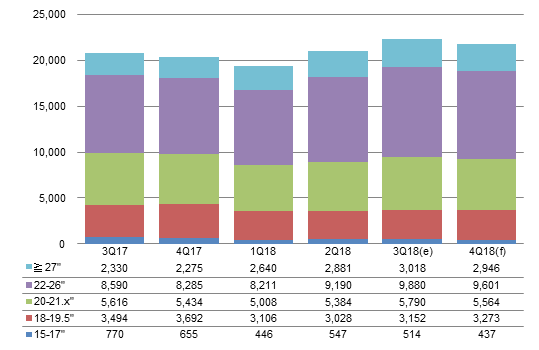

Chart 1: LCD monitor shipments, 3Q17-4Q18 (k units)

Source: Digitimes Research, November 2018

Taiwan's LCD monitor shipments grew 6.3% sequentially and 7.5% on year to reach 22.35 million units in the third quarter. (NOTE: Unless otherwise indicated, all figures and tables in this report refer to output from Taiwan makers.)

Taiwan's monitor industry has seen steady on-year growth every quarter in 2018, while the growths for the top-2 makers, TPV and Qisda, both outperformed the industry's average in the third quarter.

Although shipments will slip 2.4% sequentially in the fourth quarter due to seasonality, they will continue to increase by another 7.3% on year to arrive at 21.82 million units.

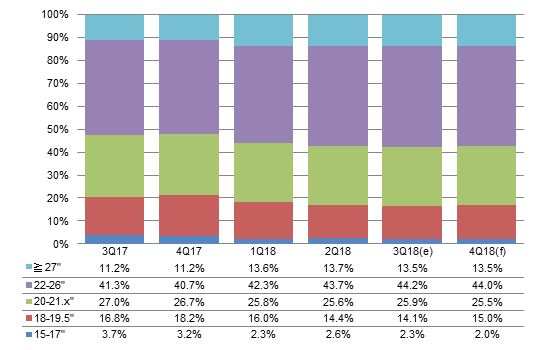

Chart 2: Taiwan's worldwide market share, 3Q17-4Q18 (k units)

Source: Digitimes Research, November 2018

Taiwan's shipments will account for around 70% of worldwide LCD monitor volumes in the second half as demand for monitors from vendors including Dell and Hewlett-Packard (HP) has been increasing, allowing Taiwan makers to expand their shipments.

Meanwhile, Korea-based Samsung Electronics and LG Electronics, which are mainly manufacturing their LCD monitors in-house, have seen weakening sales in China as their mid-range to entry-level products' price/performance ratios have been much weaker than those for Taiwan-shipped products. makers.

Although Samsung has invested additional resources into monitor development projects in 2018, the company's shipments have yet to see major improvements, and the benefits of the extra investments will not be significant until 2019.

Shipments breakdown

Production value and ASP

Chart 3: Taiwan LCD monitor production value, 3Q17-4Q18 (US$m)

Source: Digitimes Research, November 2018

Chart 4: Taiwan LCD monitor ASP, 3Q17-4Q18 (US$)

Source: Digitimes Research, November 2018

Taiwan's LCD monitor production value was up 2.8% sequentially in the third quarter, a growth smaller than that of shipments. As a result, LCD monitor's ASP slid 3.2% sequentially to reach US$106.8.

The drop in ASP was because of decreasing monitor LCD panel prices. Since the panel accounts for around 50% of a monitor's overall cost, the drop in panel prices usually has a major influence on monitor ASP.

LCD monitor panels' average price went down 1.8% sequentially in the third quarter. With the price expected to dip another 0.9-1.2% in the fourth quarter, Digitimes Research forecasts that Taiwan's monitor ASP will fall 1.5% sequentially in the quarter.

Makers

Chart 5: Shipments by top-5 makers, 3Q17-4Q18 (k units)

Source: Digitimes Research, November 2018

After enjoying a 9% on-year growth in the second quarter, TPV's shipments continued witnessing a strong on-year growth at 8.2% in the third quarter, a performance second only to Qisda.

Qisda achieved an on-year growth of 2.7% in the second quarter, but in the third quarter, its shipments went up 15% on year and 5% sequentially. Qisda's business model is mainly focusing on improving profitability and has been pushing into niche sectors such as gaming and curved products. The maker has also been keen on developing large-size monitors and its 27-inch and above monitor shipments grew 15% sequentially in the third quarter.

Samsung has become the fifth largest monitor player worldwide in the second half, falling behind LG. Samsung shipped 2.6 million monitors in the second quarter and 2.53 million units in the third. The company is expected to ship 2.42 million units in the fourth. Samsung has been outsourcing about 250,000 units to China-based BOE VT per quarter since the third quarter of 2016, and these are not included in Samsung's shipments.

LG shipped 2.51 and 2.55 million monitors in the second and third quarter, respectively, and is expected to ship 2.46 million units in the fourth quarter.

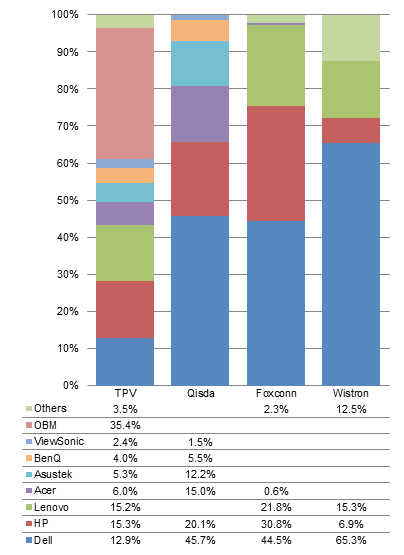

Chart 6: Top-4 makers' shipments by client, 3Q18 (k units)

Source: Digitimes Research, November 2018

Chart 7: Top-4 makers' shipments by client share, 3Q18

Source: Digitimes Research, November 2018

Chart 8: Top-4 makers' shipments by client, 2Q18 (k units)

Source: Digitimes Research, November 2018

Chart 9: Top-4 makers' shipments by client share, 2Q18

Source: Digitimes Research, November 2018

Qisda, Foxconn and Wistron's reliance on HP's orders was rising with all three makers seeing increased orders from a quarter ago in the third quarter.

Qisda's orders from Hewlett-Packard (HP) increased over 10% sequentially in the third quarter, but those from other clients mostly went down.

Foxconn's shipments to HP picked up around 3% sequentially in the third quarter, while its orders from other clients were either flat or down slightly from a quarter ago.

HP's orders to Wistron were up over 50% sequentially in the third quarter, which translates into an increase of around 40,000 units.

TPV's shipments to HP were down sequentially, but the maker saw an over 10% growth in orders from Lenovo.

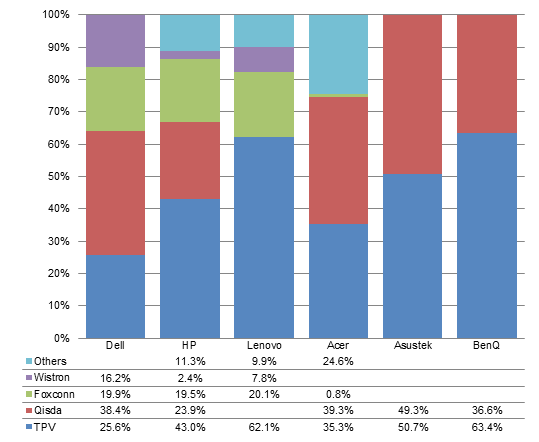

Chart 10: Major vendors' order distribution, 3Q18

Source: Digitimes Research, November 2018

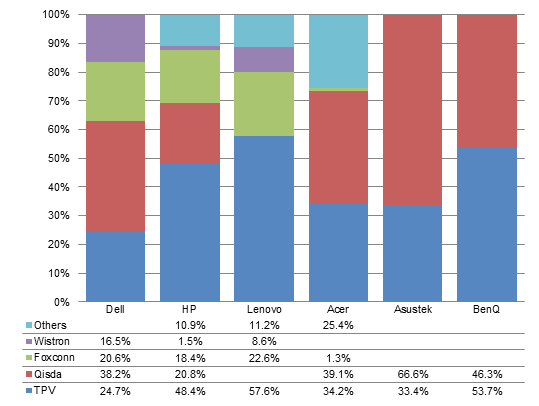

Chart 11: Major vendors' order distribution, 2Q18

Source: Digitimes Research, November 2018

HP cut its orders to TPV and increased its outsourcing to its other partners in the third quarter.

Lenovo continued raising the proportion of its outsourcing to TPV with the percentage reaching over 60% in the third quarter.

Asustek adjusted its outsourcing strategy and divided its orders more evenly between its two major partners in the third quarter.

Business models: OBM, OEM/ODM

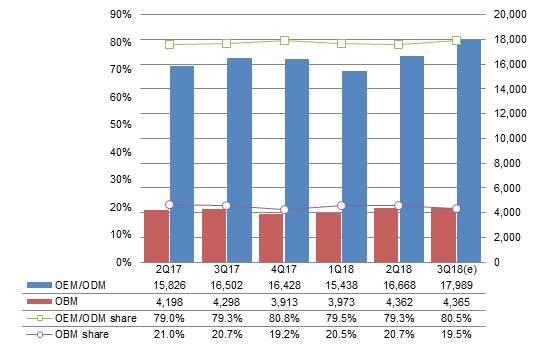

Chart 12: Shipments by business model, 2Q17-3Q18 (k units)

Source: Digitimes Research, November 2018

The share of Taiwan's OEM/ODM shipments reached 80.5% in the third quarter thanks to major increases in orders from HP and Dell, which helped boost OEM/ODM shipments by 8% sequentially.

TPV was the only maker in Taiwan with OBM shipments, with some of its major sub-brands being AOC and Phillips, and minor ones being Envision, Topview and Maya. Taiwan's OBM shipments stayed flat in the third quarter, causing their share to slip below 20%.

Screen sizes

Chart 13: Shipments by screen size, 3Q17-4Q18 (k units)

Source: Digitimes Research, November 2018

Chart 14: Shipment share by screen size, 3Q17-4Q18

Source: Digitimes Research, November 2018

Shipments in the 22- to 26-inch segment and the 20- to 21.x-inch segment both enjoyed more than 10% sequential growths in the third quarter, helping their shares rise.

Shipments of 27-inch and above models have seen their share stay consistently above 13% since first-quarter 2018.

Shipments in all segments will drop back slightly from a quarter ago in the fourth quarter except 18- to 19.x-inch models, as Taiwan makers will aggressively promote these monitors to emerging markets.

Annual shipments

Chart 15: Taiwan and worldwide LCD monitor shipments, 2014-2018 (k units)

Source: Digitimes Research, November 2018

Taiwan's shipments in 2018 are expected to rise 5.8% to 84.62 million units.

Worldwide shipments will achieve its first on-year growth since 2012 at 1.8%.

Taiwan's share will also rise from 66.3% in 2017 to nearly 69% in 2018.

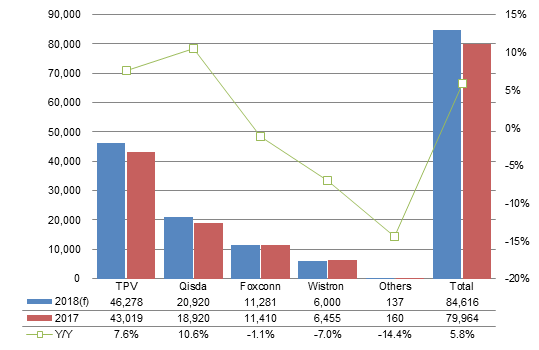

Chart 16: Shipments by top makers, 2017-2018 (k units)

Source: Digitimes Research, November 2018

Despite its priority given to profitability, Qisda will be the only maker to achieve on-year growths five years in a row and will also be the best preforming maker in Taiwan in 2018 with an over 10% on-year increase.

TPV's shipments will also pick up 7.6% on year to climb back to above 46 million units in 2018.

Article translated by Joseph Tsai and edited by Rodney Chan